There is a limit to how much a homeowner can borrow with an FHA loan, a type of mortgage guaranteed by the Federal Housing Administration. FHA Loan limits in Texas are based on a percentage of the median home price in each county if you want to buy a home with a FHA Loan.

Government guarantees on these mortgages are intended to help low- to moderate-income borrowers who might otherwise be shut out of the housing market, but they shouldn’t burden taxpayers with extravagant purchases. This loan guarantee can make FHA loans a little more expensive than conventional loans. Texas borrowers have to pay upfront mortgage insurance, as well as monthly mortgage insurance premiums—potentially for the life of the loan.

What is FHA Loan Limit

The FHA loan limit is the maximum amount you can borrow. There are different limits depending on the type of property you intend to purchase (e.g. single-family properties have lower limits than multi-family properties). Check out today’s Texas FHA Rates and calculate mortgage payments.

Getting an FHA loan does not automatically allow you to borrow up to your county’s limit. Based on your income, credit score, and other factors, you can only borrow as much as you qualify for. Furthermore, the loan amount cannot exceed 100 percent of the appraised value of the property.

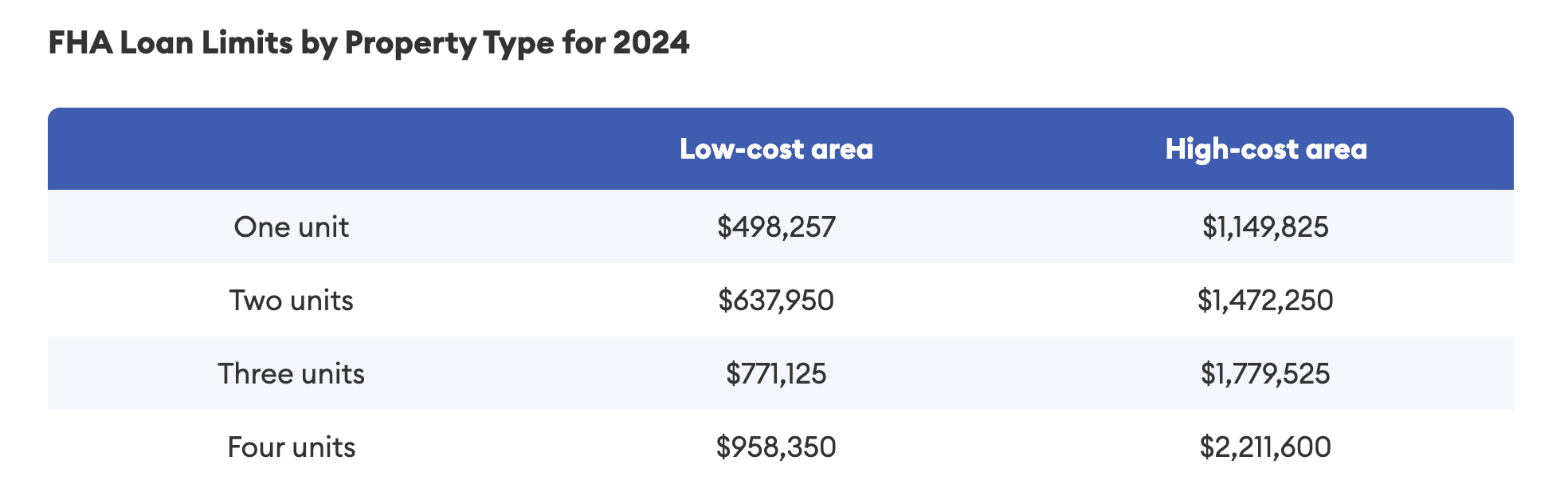

Texas FHA Loan Limits by Property Types

One-unit properties in low-cost areas are eligible for an FHA loan limit of $498,257 for 2024. A one-unit property in a high-cost area is eligible for an FHA loan limit of $1,149,825. This is called the nationwide loan limit “floor.” The nationwide loan limit “ceiling” falls between these two limits. Several hundred counties have limits somewhere in between.

There are different Texas FHA loan limits by types of properties. The lowest rates apply to one-unit properties, the highest rates apply to two-unit properties, the highest rates apply to three-unit properties and the highest rates apply to four-unit properties.

Texas FHA loans are more expensive if you want to buy a duplex than a single-family home. In addition, if you live in one of the units as your primary residence, you can obtain an FHA loan for a multi-unit property.

FHA vs. Conforming Loan Limits

FHA loans aren’t as flexible as conventional loans. If you want more money, you’ll need to qualify for a conventional loan. The FHA will consider your application even if you have bad credit—a score of 500 or lower—if you can put down 10%. The down payment can be as low as 3.5% if your credit score is 580. As low as 3% down payment is possible with a credit score of 620.

Conventional loans give you access to loan limits that are within the conforming loan guidelines. For you to qualify, your finances will need to be strong, and your home’s appraisal value must support your loan amount. You may, however, be able to buy a much larger home if you have access to a higher loan limit.

Frequently Asked Questions

Do Texas FHA loans have an income limit. What is it?

Although Texas FHA loans do not have minimum or maximum income limits, they are intended for low- to moderate-income Americans who cannot qualify for conventional financing or afford the down payment required for other types of loans.

The maximum loan limit for Texas FHA loans is determined by what factors?

In addition to the county in which you live (and the home values within it), there are additional factors that influence the maximum Texas FHA loan limit. The FHA loan limits will be higher in high-cost areas and in multifamily properties that are larger and more expensive.

How do you find Texas FHA loan limits for your area?

You can find out the FHA loan limits in your area by using the Department of Housing and Urban Development’s FHA Mortgage Limits search tool.